Office lease renewal: 7 data points for CFOs decide whether to renew or relocate

TL;DR

To make a defensible office lease renewal decision, you need 7 categories of utilization data: daily occupancy rates by day of week, desk no-show rates, peak day demand, team attendance patterns, market rent benchmarks, a total occupancy cost model, and lease accounting sensitivity checks. Without this data, you are committing to a multi-year cost based on assumptions that may already be wrong.

Most companies renew their office lease based on headcount projections and last year's attendance patterns, then spend the next five years paying for space their teams no longer use. Before your CFO signs a multi-year commitment, they should ask for seven specific data points that reveal whether you need more space, less space, or just better coordination across the days your teams already come in.

Renew, renegotiate, or relocate for an office lease

When your lease expires, you face 3 options: renew at current terms, renegotiate with your landlord, or relocate to a different space. Each path carries different costs, risks, and timelines. Your CFO needs concrete data to evaluate which option makes financial sense.

Renewing keeps things simple. You avoid moving costs and disruption. The risk? Locking into a space that no longer fits how your teams actually work.

Renegotiating lets you adjust terms, size, or rate with your current landlord. This works well when you have utilization data showing you need less space. Landlords prefer keeping tenants over finding new ones, so you often have more leverage than you think.

Relocating gives you a fresh start with a space designed for your current needs. The tradeoff is significant: buildout costs, moving expenses, and productivity loss during the transition that needs to be planned thoroughly. For a company with 1,000 employees, this can easily add millions to the total cost.

[Table2]

When should you start planning for an office lease renewal?

Start your planning 18 to 24 months before your lease expires. This timeline gives you enough runway to gather data, evaluate options, and negotiate from a position of strength.

Your lease contains critical dates you cannot miss.

- The notice period is the window in which you must tell your landlord whether you plan to stay or leave. Miss this deadline and you lose negotiating power.

- The option window works differently. If your original lease includes a renewal option at a predetermined rate, you must exercise it within a specific timeframe. Let that window close and you lose the option entirely.

- Holdover is what happens when you stay past your expiration without a new agreement. Most leases impose steep penalties for holdover, sometimes double your normal rent. This is why starting early matters so much.

Market benchmarks and lease comps for a renewal negotiation

You cannot negotiate effectively without knowing what other companies pay for similar spaces. Your landlord knows the market, you should too. Lease comps are recent signed deals in your area, showing the actual rates other tenants secured rather than the asking prices landlords advertise. This data tells you whether your renewal offer is fair.

Effective rent is the true cost after accounting for concessions. A landlord might offer 2 months of free rent or a tenant improvement allowance for buildout. These concessions reduce your effective rate below the stated base rent.

Vacancy rates in your submarket directly affect your leverage. When lots of space sits empty, landlords compete for tenants. When space is tight, you have less room to negotiate. Check current vacancy rates before you start any commercial lease renegotiation.

Total occupancy cost beyond base rent

Base rent is the number everyone focuses on. It is also incomplete. Your CFO needs to see the total occupancy cost to compare renewal against relocation accurately.

[Table1]

Operating expenses can escalate every year, and your lease specifies how these pass-throughs work. Some leases cap annual increases. Others do not. Read the fine print.

Buildout costs for a new space can average $280 per square foot. For a 40,000 square meter office, this adds up fast. Your landlord may offer a tenant improvement allowance, but it rarely covers the full cost.

Moving costs go beyond hiring movers. You lose productivity during the transition. IT systems need reconfiguration. Employees need time to adjust. These soft costs are real even if they do not show up on an invoice.

Scenario planning models for a lease decision

A 5-year lease signed on today's assumptions can look very different by year 3. Before your CFO commits, you need models that stress-test the decision against futures you don't control.

Run 3 cases. The base case holds your current headcount and hybrid patterns steady. This is your starting point, not your answer. The downside case models what happens if remote adoption increases or headcount shrinks: fewer people in, less space needed, and a lease that suddenly looks 30% too large. The upside case models faster-than-expected hiring: will your space absorb the growth, or will you be scrambling for additional floors at whatever the market charges that year?

Each model is only as good as its inputs. If your attendance data comes from badge swipes or manual headcounts, your scenarios are built on guesses. You need to know how your teams actually use the space today: which days, which floors, which teams. That is what makes the difference between a scenario your CFO can defend and one they cannot.

The 7 data points your CFO should ask for before you renew the lease

These 7 data points transform a lease renewal from a gut decision into a defensible recommendation. Gather this information before your CFO signs off on a multi-year commitment.

1. Space utilization and occupancy rates by day

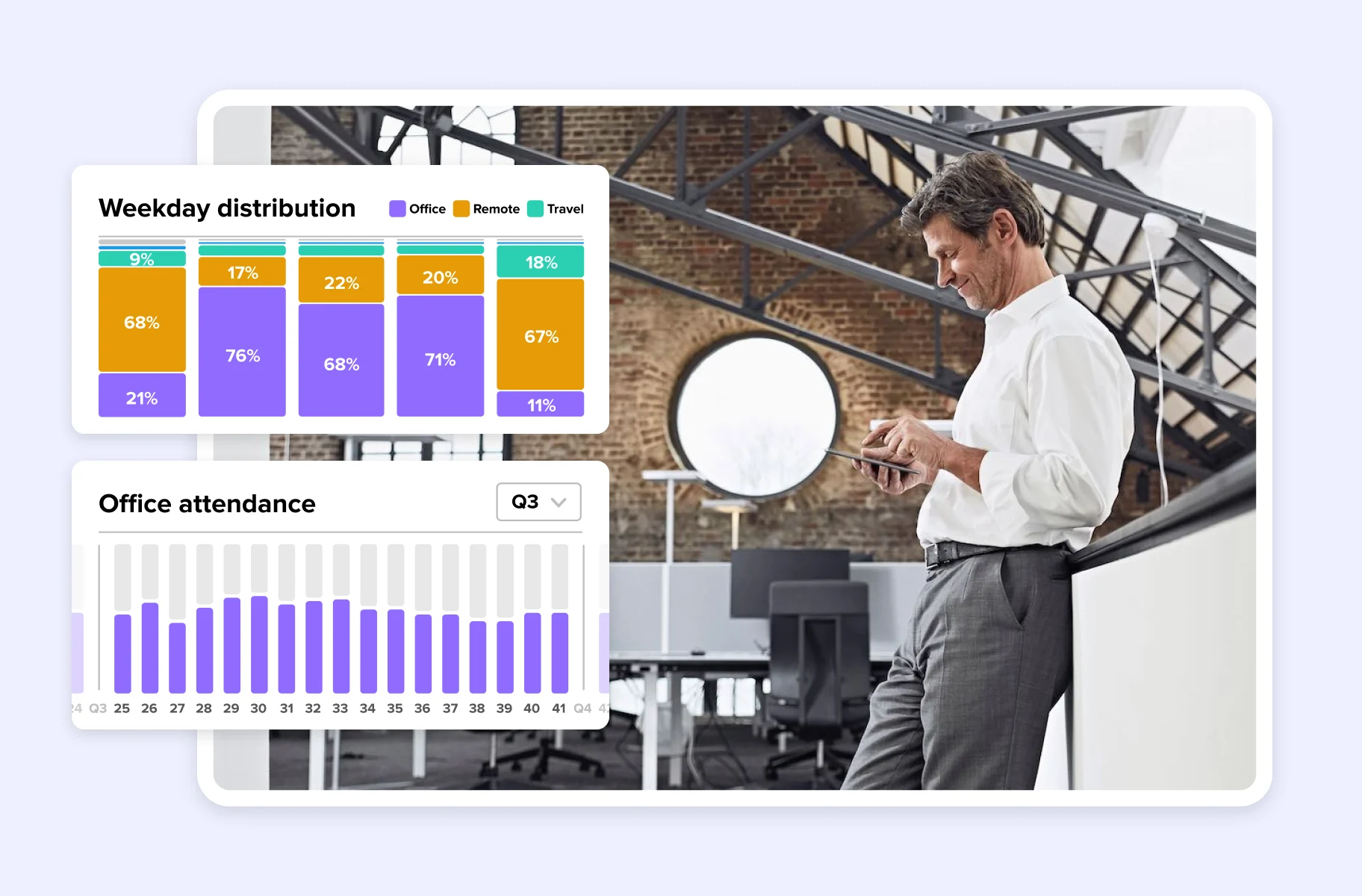

Space utilization measures desks used compared to desks available. This sounds simple, but most companies get it wrong.

Monthly averages hide the reality of hybrid work. Your office might show 50% average utilization, but that number masks extreme daily variation. Tuesday could be at 90% while Friday sits at 15%. If you base your lease decision on the average, you will either overpay for empty space or leave employees scrambling for desks on busy days.

Your CFO needs the daily breakdown. This data shows whether you can reduce your footprint or whether you need every desk you have.

2. Desk and meeting room no-show rates

A no-show happens when someone books a desk or meeting room and does not show up. This is more common than most companies realize.

High no-show rates inflate your apparent demand. If your booking system shows full occupancy but half those desks sit empty, you are making decisions based on fiction. The gap between bookings and actual check-ins is the data your CFO needs to see. Tracking no-shows requires a system that confirms arrival. Without check-in data, you are guessing.

3. Peak day demand and capacity risk

Average utilization is dangerous because it ignores peak days. If 800 people show up for 500 desks on a Wednesday, your employee experience suffers immediately.

Your CFO needs to know your maximum peak demand, as this number determines the minimum space you can lease without creating daily chaos. It also informs whether you need to implement team schedules to spread attendance more evenly across the week.

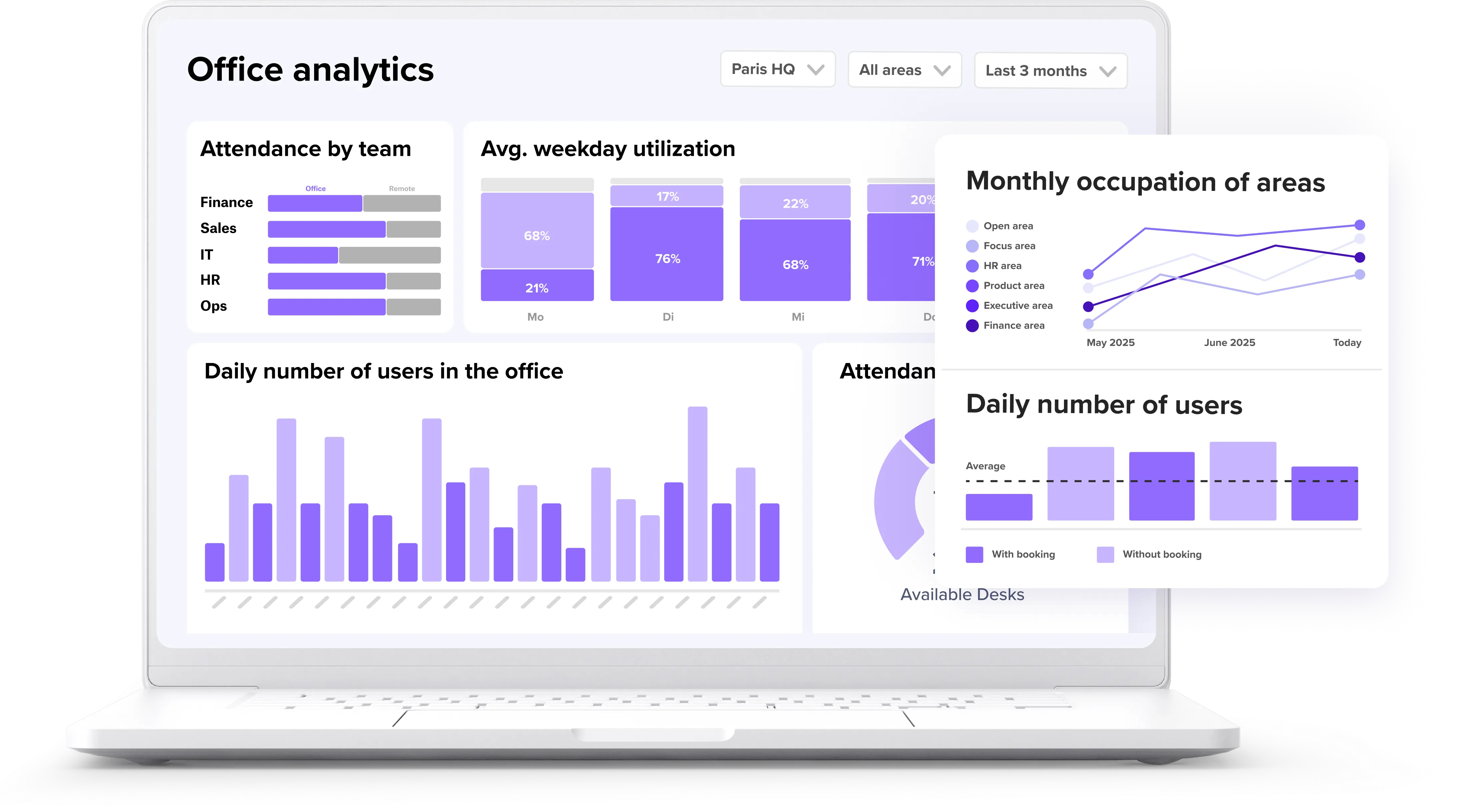

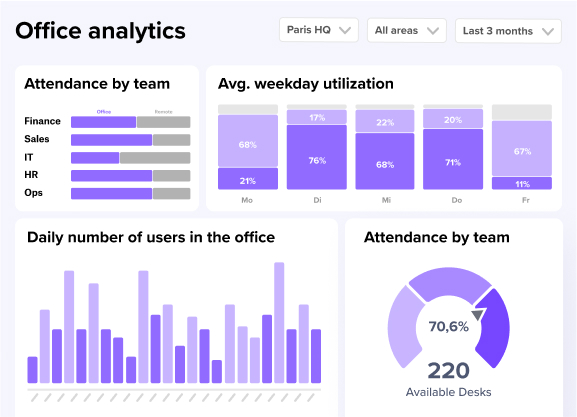

4. Team attendance patterns and hybrid policy adherence

Which teams come into the office? When do they come in? Do they overlap with the teams they need to collaborate with? Team-level data reveals whether your floor plan supports how people actually work. If engineering and sales never overlap, you might not need a dedicated desk for every person. If product and design always come in on the same days, you need enough space to accommodate them together.

This data also shows whether your hybrid policies are actually followed. If leadership mandates 3 days in the office but data shows an average of 1, your CFO needs to know before signing a lease based on a policy no one follows.

5. Market rent benchmarks and tenant incentives

Internal utilization data tells half the story. External market data completes it. Compare your current asking rent against recent lease comps in your submarket. If market rents have dropped, renewing at your current rate is a mistake. If vacancy rates are high, you can demand better concessions. This external data provides the leverage you need for a successful negotiation.

Your negotiating power depends heavily on where you are though. According to Cushman & Wakefield's 2026 data, US office vacancy sits at 20.2%. In most submarkets, landlords need tenants more than tenants need a specific building. In the UK, the picture splits: London vacancy has fallen to 7.4% in 2026 (down from 10.6% in 2025) limiting leverage on Grade A space. Regional cities sit closer to 10.8%, where conditions are more negotiable. Wherever you are, your landlord already knows the local vacancy rate. The question is whether you walk in with your own utilization data to match it.

6. Total occupancy cost model with buildout and moving costs

Comparing base rent between two buildings is a flawed approach. Your CFO needs a model that includes operating expenses, buildout costs, and moving expenses. Relocating to a smaller, cheaper office might actually cost more once you factor in construction and transition expenses. Present a total occupancy cost model that shows the full financial picture over the lease term.

7. Covenant and lease accounting sensitivity checks

A commercial lease renegotiation affects your balance sheet. In the US, under ASC 842 lease accounting standards, you must record the right-of-use asset and lease liability for your office space. These lease accounting changes affect financial ratios and can trigger issues with debt covenants.

Your CFO must run sensitivity checks to see how a new lease alters your financial position. Tracking these liabilities in spreadsheets creates audit risk. You need precise data and proper systems to ensure your real estate decisions do not create problems elsewhere.

How workplace analytics support lease decisions

You cannot make a confident lease decision without accurate utilization data. The challenge is getting that data in the first place.

Spreadsheets and manual headcounts do not scale. They create version control problems, audit risks, and data gaps. For a company with 1,000 employees across multiple floors, you need a system that captures attendance and space usage automatically.

A workplace management platform like deskbird provides this data directly. Because it integrates with MS Teams, Outlook, and Slack, employees book desks and check in through tools they already use. That matters more than it sounds.

Most booking tools track intent. deskbird tracks what actually happens. Without check-in confirmation, your no-show rate is invisible and your occupancy data is a guess. With it, your CFO has numbers they can defend in a board-level real estate conversation.

deskbird customers report a 90%+ adoption rate across their workforce, the highest in the market. High adoption is what makes the data accurate. Facilities teams using deskbird's utilization data reduce their leased space by 20–30% on average. That is a real estate decision your CFO can justify.

For IT, there is no maintenance burden: SCIM auto-provisioning, SSO, and zero-touch setup. Built and hosted in Germany, with ISO 27001, SOC 2 Type II, and full GDPR compliance included.

If your lease clock is ticking, book a demo to get CFO-ready utilization data.

Frequently Asked Questions

How far in advance should you start planning a lease renewal?

When is it better to renegotiate an office lease than to relocate?

Renegotiation makes more sense when your utilization data shows you need less space than you currently lease, your landlord has high vacancy in the building, and your fit-out is already sunk. Relocation only wins financially when your current space is structurally misaligned with how your teams work and the total occupancy cost over the new lease term, including buildout and transition, comes in lower than staying. Run both scenarios with full cost models before deciding.

Why do monthly utilization averages mislead CFOs?

What is the difference between asking rent and effective rent?

Asking rent is the stated price per area (square meters/foot). Effective rent is the true cost after accounting for concessions like free rent months or tenant improvement allowances. Always negotiate based on effective rent.

How do I calculate office utilization rate?

Get the utilization data your CFO needs before signing

- See daily occupancy, no-show rates, and peak demand in one place

- Accurate data means your CFO can defend every number before signing

- 90%+ adoption rate across 500+ companies means the data you get is reliable